Monnari Trade (WSE: MON): Investing in a Polish Microcap Fashion Company

Monnari Trade (WSE: MON): Investing in a Polish Microcap Fashion Company

Small company with a very solid balance sheet, a management team with "skin in the game," and growth potential

Investment thesis in a nutshell

Monnari Trade, a Polish fashion company with a relatively low market capitalization, is currently trading at a substantial discount to its book value. Its present market value of 37 million euros is a 40% markdown from its book value of 60 million euros (Price-to-Book Ratio = 0.6x).

This discount can be attributed to various factors, including declining operating margins, uncertainty in the fashion business, and the company's competitive position. Nevertheless, the company boasts a robust balance sheet with 33 million euros in current assets and 15 million euros in real estate investments, which are presently not factored into the stock price.

This significantly mitigates the company's risk, even in a conservative scenario.

Taking these factors into account, I project a target stock price of 9.7 zlotys, signifying a potential upside of 80%.

Disclaimer: This website and/or article do not provide any investment recommendations. Nothing included should be considered a basis for making investments or decisions. The information contained in the website/article is for informational and educational purposes only. Prior to making any investment decisions, it is advisable to seek appropriate professional advice and conduct your independent analysis. You bear full responsibility for your investment choices.

Monnari’s business

Monnari Trade is a Polish fashion company that operates in the clothing distribution sector. The company is primarily engaged in designing clothing but does not handle its manufacturing.

Monnari's business model focuses on targeting women aged 30 and older, primarily through traditional retail stores. Since its establishment in 1998, Monnari has emerged as a prominent fashion brand in Poland, boasting a network of over 225 stores throughout the country.

Monnari generates revenue through several channels:

Retail Sales: Approximately 80% of its sales come from the traditional brick-and-mortar retail stores. These physical stores are a key source of revenue, serving as a direct point of contact with customers.

Online Retail: Monnari also conducts around 17% of its sales through online retail channels. This includes e-commerce platforms where customers can browse and purchase clothing from the comfort of their homes.

Wholesale: A smaller portion, approximately 3% of the company's sales, comes from wholesale distribution. Monnari sells its clothing products to other retailers or businesses on a wholesale basis.

Monnari’s brand and production

Monnari outsources the production of its clothing to factories in China and other Southeast Asian countries. The company maintains a design office in Poland, responsible for developing clothing collections. As a result, clothing is manufactured in the contracted factories in line with Monnari's designs.

Outsourcing production enables Monnari to focus on product design and marketing while sparing the company the complexities of production. This strategy allows for resource allocation to other areas of the business.

Outsourcing production is a common practice in the fashion industry. Most fashion companies outsource their product manufacturing to factories worldwide, primarily in China, India, Southeast Asia, and Turkey.

Ownership structure

Monnari is a company where the founder has a lot at stake: CEO and founder Miroslaw Misztal owns over 33% of the company. This is a strong indicator, as he has significant money invested (>€10 million) compared to his salary.

The company also holds 4.6 million shares in treasury out of a total of 30.6 million, valued at over €5 million, a result of a buyback program. While there is no official confirmation, these shares are not expected to return to the market, although it would go against the current company policy and be akin to a capital increase.

In addition, in late March, the CEO purchased an extra 1% of shares, 300,000 shares, at an approximate cost of €350,000, demonstrating his commitment to the company. Remember the words of Philip Fischer: "There are many reasons for insiders to sell, but few when they buy." Furthermore, the company has initiated a share buyback plan, which is uncommon in Poland.

The Clothing Sector in Poland

Sector Size

The clothing sector in Poland is valued at approximately 100 billion zlotys (25 billion euros) in 2023. The sector comprises a wide range of businesses, from large multinational corporations to small family-owned enterprises, which is quite typical in Poland.

Distribution accounts for 40% of the sector, equivalent to around 10 billion euros.

Promising Growth Prospects

Poland boasts a young and expanding population with increasing purchasing power and prosperity. Furthermore, the country is well-positioned to tap into global fashion trends such as sustainability and "fast fashion." Consequently, all studies indicate a favorable growth potential for the clothing sector in Poland.

High Competition, Risks, and Market Structure

Monnari faces intense competition in Poland's women's fashion sector. Key competitors include:

Reserved: Poland's largest fashion brand with a diverse product range encompassing clothing, accessories, and footwear.

Mohito: A youthful and contemporary fashion brand with a focus on urban style.

House: A casual fashion brand emphasizing comfort and versatility.

Cropp: An urban fashion brand with a focus on bold and avant-garde style.

Sinsay: An affordable fashion brand offering a wide range of products for all occasions.

These companies compete with Monnari based on factors such as price, quality, design, and location. Monnari distinguishes itself by focusing on classic and elegant fashion. However, Monnari is significantly smaller than its competitors, holding a market share of approximately 1% in the distribution market in Poland.

While the company's market share has slightly declined in recent years, Monnari has adjusted its strategy to remain competitive. It has expanded its product range to include men's and children's clothing, broadening its market. Additionally, Monnari has opened new stores in Poland and abroad. Nevertheless, there are reasonable doubts about the business's future and Monnari's competitive position. Overall, the market may be expanding, but margins are (and are likely to remain) thin.

Evident risks include zloty depreciation (Monnari sources everything externally), inflationary pressures (unfavorable for costs), fierce competition that could further erode margins, and the risk of a recession.

Valuation

Three main cases based on liquidation value, discounted cash flows and multiples are presented:

Liquidation value (selling all company assets)

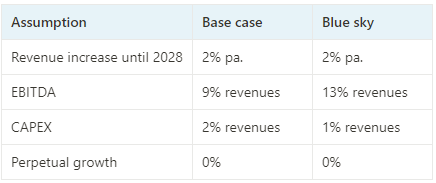

Base case and blue-sky scenarios using discounted cash flow and terminal value (estimating results and discounting future years at a rate that reflects our cost of capital and business and country risk). We will estimate for 4 years and add the terminal value of the business.

Base case and blue-sky scenarios using multiples, including real estate significance.

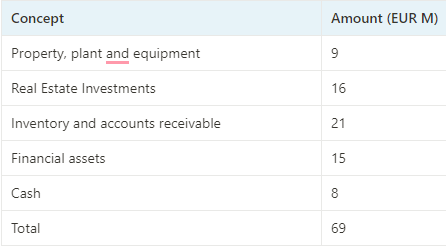

Liquidation value

Monnari boasts a very strong balance sheet. It holds no debt and maintains a cash position of 8 million euros. Additionally, we must consider financial assets (invested funds) worth 10 million euros. Furthermore, Monnari holds a substantial inventory and real estate assets.

To this, we should subtract a sum of 12 million euros in short and long-term liabilities, which, when combined with other minor discrepancies due to taxes, would yield a book value of 60 million euros. Therefore, compared to the market capitalization, we are talking about a 40% margin (60 million euros / 37 million euros). Without taking inventories into account (assigning them a value of 0 euros), we would still be looking at a 5-10% margin.

All of this is without considering that this figure includes 5 million euros that are being deducted due to the buyback program.

As we mentioned earlier, the most interesting aspect of the company lies in its real estate investments. The main investment, "Geyer's Garden," is an 11-hectare property, of which 6 hectares have already been sold. The 2022 sale generated profits of around 9 million euros and had a total value close to 20 million euros. In the first-half report of 2023, Monnari details that the remaining 5 hectares are ready for sale, valued at 16 million euros on the balance sheet. However, considering inflation and the previous sale, the property might be slightly undervalued.

Discounted Cash Flow (DCF)

Discounted cash flow involves making an estimate of the company's business and calculating a terminal value based on a discount rate (future cash flows are worth less than present ones).

In the first half of 2023, Monnari had an EBITDA of 7 million zlotys compared to 142 million in revenue. Its EBITDA margin would be around 5%. If we use a 5% EBITDA on revenue, we would obtain a value very close to the current stock price. For the base case, I use 9%, closer to the historical average. For the "blue sky" case, I use 13%. Consider that in 2019, before COVID, the company's margins were around 10%. In the upper case, we add back amortization to the EBIT margin to return to EBITDA, which is closer to operational cash flow.

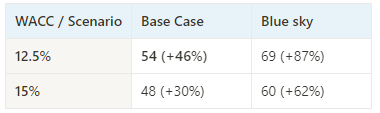

Current Market Capitalization: 37 million euros

Market Capitalization Scenarios based on WACC (cost of capital) and assumptions in the table above (revaluation vs. current market value in parentheses):

To these values, we would need to add the non-productive assets included on the balance sheet. In my opinion, at least 50% of financial assets, leaving the real estate as potential upside. Thus, we would be at a level of 54 million euros:

Multiples and Balance

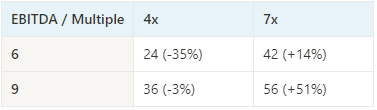

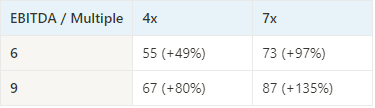

We start with the scenarios mentioned above (9% and 13% EBITDA) with approximate revenues of 300 million Zlotys. This would give us an EBITDA of 27 to 39 million Zlotys (6 to 9 million euros).

For a business like this, exposed to economic downturns, I have selected a conservative multiple of 4x. A multiple of 6-7x wouldn't seem unreasonable in a more favorable situation.

To these multiples, we must add the excess of financial assets. And in this case, we will also reflect the value of the balance sheet with the real estate assets and the overall excess cash. Value based on multiples without considering the balance sheet:

If we add 16 million euros for the real estate assets and 15 million for financial assets, we get the following:

Valuation Summary

Based on all of the above, I estimate a market capitalization of 65 million euros (295 million Zlotys), which would imply an 80% upside (current share price of 5.4 PLN compared to estimated 9.7 PLN).

Conclusion

Monnari Trade offers an intriguing value proposition with a significant margin of safety. It possesses a strong balance sheet, a solid business, and a series of short-term catalysts that could boost its stock price.

The substantial discount to book value, along with the clothing business generating a substantial cash flow, opens the door to other catalysts, such as share buybacks. The target price should increase with the expected buyback program. The appreciation of the Zloty could also benefit Monnari Trade since its clothing manufacturing takes place abroad.

Furthermore, the real estate assets and Monnari Trade's overall balance sheet represent a significant value for the company, which the current stock price does not fully factor in and would limit potential losses for an investment.

While the competitive environment and macroeconomic conditions introduce certain risks, I believe Monnari's position equips it well to thrive in this ever-evolving landscape.