Investing in graphite and titanium - Sovereign Metals (ASX: SVM)

Investing in graphite and titanium - Sovereign Metals (ASX: SVM)

World-class graphite and titanium deposit and partnership with Rio Tinto, one of the leading mining companies globally

The following investment thesis is available in Spanish via video at Locos de Wall Street. Visit the link below and register to access: https://locosdewallstreet.com/2024/05/descubre-la-empresa-que-podria-ser-la-nueva-adriatic-metals/

Investment Thesis in a Nutshell

Sovereign Metals (ASX: SVM), an Australian mining company, is driving the development of the vast Kasiya deposit in Malawi, which contains significant quantities of rutile (a titanium ore) and graphite. A final investment decision is expected in 2025, with production anticipated in 2027/28. The thesis can be summarized in the following six points:

Debt-Free Structure and Attractive Current Market Value vs. Net Asset Value (NAV): Approximately 10% ($160M vs. $1600M; $160M vs. $1,000M if Rio Tinto exercises its rights), plus cash value vs. market value of 25% ($40M vs. $160M).

Valuation in Line with Competitors: After reviewing a group of 10 competitors, undeveloped projects with potential trade at 15-20% NAV, and mature, funded projects at least 50% NAV.

Critical Metals for the Energy Transition and Preliminary Study Completed: Titanium and graphite are essential for clean energy, decarbonization, and high-tech industries.

World-Class Asset: Kasiya will be a top global producer of graphite and titanium in terms of both quantity and cost. It is one of the largest known rutile deposits, from which the purest and most cost-effective titanium can be extracted.

Political Support and Involvement of Rio Tinto: One of the world's leading mining companies, Rio Tinto, has the capacity to absorb the operation and potentially acquire the entire SVM once the mine is developed.

Considering Malawi's Risk, but High Deposit Quality: Conservatively, it should trade around 50% NAV upon completion of the definitive study and securing financing (12-18 months if all goes well). Here are the figures:

Current Market Cap: AUD$275M

Pre-Financing Target Market Cap: AUD$400M

Post-Financing and Near-Construction Target Market Cap (assuming the feasibility study yields similar results to the preliminary study): AUD$1000-1200M

Potential 3x-4x increase in 4 years. Re-rating from a developer to a producer.

Finally, if you're wondering why it's trading at a discount... it's straightforward: jurisdiction (Malawi) and uncertainty about actual resources and final project financing. That’s it.

Disclaimer

This website and/or article does not provide any investment recommendations. Nothing contained herein should be construed as a basis for making investments or taking any actions. The information contained on the site/article is purely for informational and educational purposes. Before making any investment decisions, you should seek appropriate professional advice and conduct your own analysis. You are fully responsible for your investment decisions. The author of the article is a shareholder in the company.

Sovereign Metals and the World-Class Kasiya Deposit

Sovereign Metals is an Australian mineral exploration company focused on discovering and developing critical mineral deposits. The company’s flagship project is the Kasiya Project, located in Malawi. Sovereign Metals is listed on both the Australian Securities Exchange (ASX: SVM) and the AIM market of the London Stock Exchange (AIM: SVML). The company currently has a market capitalization of AUD$280 million (US$175 million).

SVM's plan is clear: develop the Kasiya deposit at the lowest possible cost and exploit it, especially considering the demand for its two main metals, titanium and graphite.

In September 2023, the company published its Pre-Feasibility Study. This study determines if it makes sense to continue investing money and developing the mine based on the projected value of its resources. The answer is clear: yes. Though not certain, the results are extremely promising:

Net Present Value (NPV): $1600M

$600M development and construction expenditure before production

Internal Rate of Return (IRR): 28%

Average EBITDA: $400M, $25,000M in revenue over the mine's lifespan

Annual average production of 222,000 tons of rutile and 244,000 tons of graphite, with a 25-year mine life

Enormous deposit - initially, only 30% of the known mineralization would be extracted to avoid flooding the market. It is the largest rutile discovery in 70 years and the second-largest graphite deposit globally.

This is the Pre-Feasibility analysis, with the definitive study expected in mid-2024. This will be a crucial moment, especially considering Rio Tinto's role.

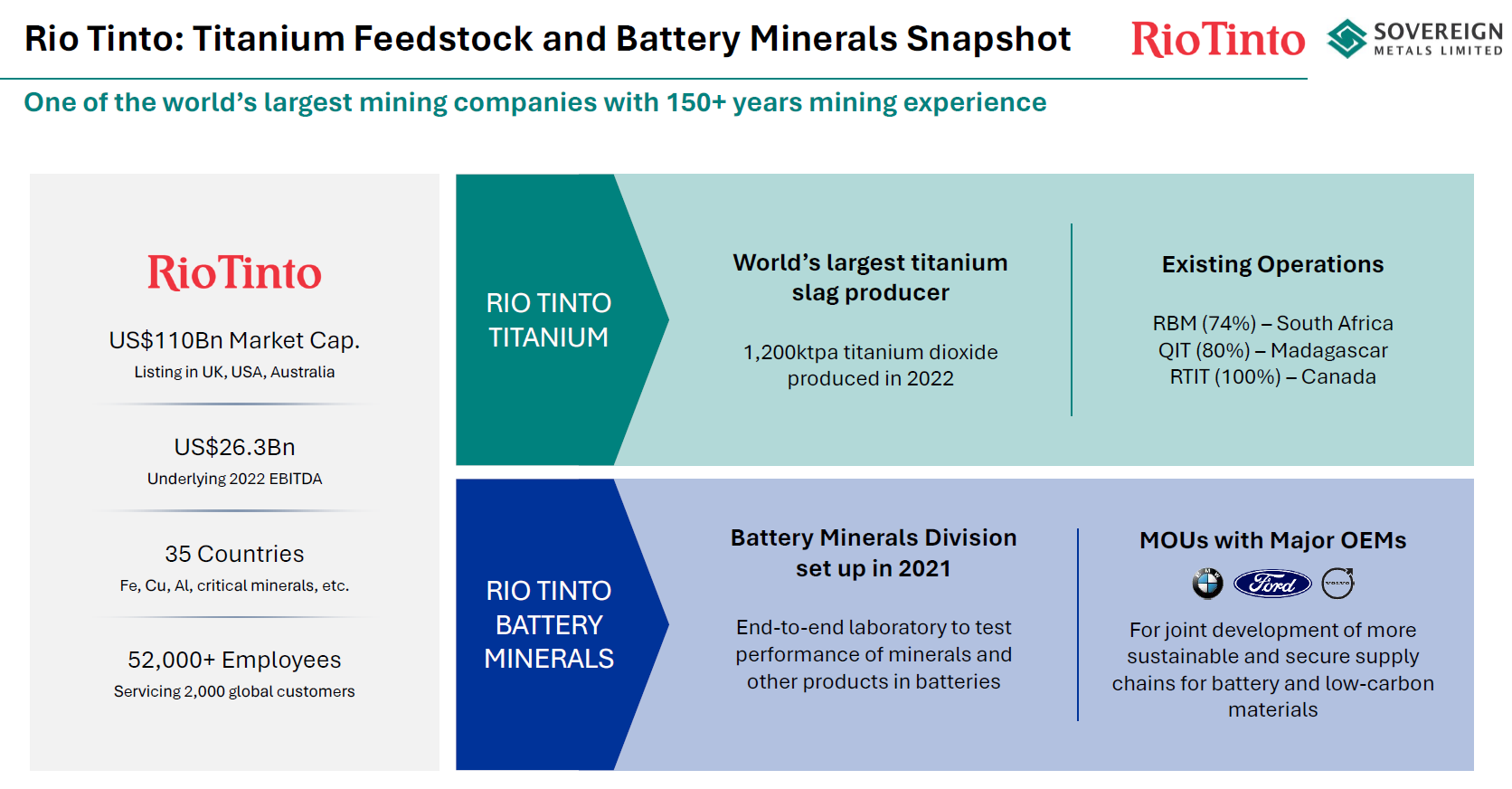

Rio Tinto: The Major Shareholder

Rio Tinto holds a 15% stake in SVM and is the world's leading titanium producer, as well as one of the largest mining companies globally. This ensures robust commercialization of all production from Kasiya, signaling significant potential for this project.

Rio Tinto's Investment Phases:

July 2023: Rio Tinto acquired 15% of SVM for AUD 40M at AUD 0.48 per share (currently at AUD 0.48).

July 2024: Option to acquire an additional 4.99% at AUD 0.53 per share.

July 2024 - July 2025: Final feasibility study, financing negotiations, and Rio Tinto's right to become the mine operator upon completion of the study (with rights to market 40% of production).

Management owns approximately 10% of the company, with the remainder held by various funds, significant Australian investors, and free float. This ownership structure is promising.

The role Rio Tinto decides to play in 2024 and 2025 will be crucial. Regardless, the investment choice appears clear.

Path to Production: Key Milestones

2023: Pre-feasibility study and initial investment by Rio Tinto.

2024: Final feasibility study and Rio Tinto's investment decision.

2025: Start of construction.

2027/28: Commencement of production.

Why Titanium and Graphite?

The two primary metals in the deposit are graphite and rutile (a titanium mineral). These metals are critical for the next 20 years, making it vital for the USA and Europe to secure supplies. Rio Tinto is well-positioned to lead this effort.

Titanium:

China controls approximately 35% of the world's titanium, while the USA has very little (almost 0%), relying heavily on other countries, particularly Japan.

Titanium is primarily used in the manufacture of armaments, robots, ships, and missiles. The key point is that titanium is essential for the future, and its price is likely to increase given expected demand and existing deposits.

The Kasiya deposit is particularly noteworthy because it primarily contains rutile. Natural rutile is the purest and highest quality form of titanium dioxide (TiO2), and is the preferred raw material for producing titanium pigments and metallic titanium. Kasiya is the largest rutile deposit discovered in 70 years.

The supply of high-quality titanium raw materials is scarce and diminishing. The new projects set to launch in the short and medium term are limited. Therefore, my opinion is clear: relative prices can only continue to rise.

Graphite

Graphite is critical for lithium-ion batteries. The main use of these batteries, apart from the obvious industrial level, is in electric cars. For me, this is the key, even more than the titanium aspect.

With the energy transition, the demand for graphite can only grow. Each electric car requires at least 40kg of graphite, for example. The International Energy Agency (IEA) forecasts that graphite demand will increase 8 to 25 times from 2020 to 2040.

And here’s the kicker. China holds about 60-70% of the known reserves, while the USA and Europe are struggling to keep up. Again, looking at the graph below, my opinion on prices is obvious.

Logistics, Geopolitics, and Jurisdiction (and the Risks of Investing in Malawi)

Investing in Sovereign Metals involves certain risks, especially considering its location in Malawi and the nature of the mining industry.

Firstly, investing in a developing country like Malawi involves political and regulatory risks. Although there haven’t been significant issues in recent years, it's a factor to consider.

Secondly, on a logistical level, the project has its complexities. The mineral would be transported to the ports of Nacala and Beira.

Thirdly, we are currently in a global war over key minerals. China and the USA are playing this game strongly, which could have consequences, placing projects like this right at the heart of the issue.

Other evident risks include:

Geological and Technical Risks: In the exploration and development of mines.

Resource Risk: The real resource might differ from initial studies.

Price Volatility: Prices of metals and minerals can be volatile, though mitigated through various pre-agreements and Rio Tinto’s network.

Production Cost Fluctuations: Always a risk.

Financing: Not secured and crucial, to be negotiated with Rio Tinto.

Valuation

Price to NAV Ratio The case for SVM is a re-rating of the discount on the value of the mine once constructed (Price to NAV ratio). To do this, we will calculate the NAV (Net Asset Value) via discounting future cash flows, assigning a percentage based on the current stage of the project.

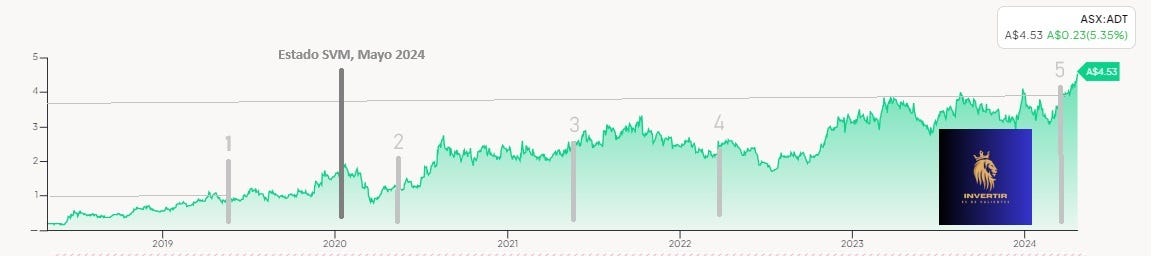

Despite significant differences in metal, jurisdiction, and management, the case bears some parallels to Adriatic Metals about 5 or 6 years ago.

Between step 1 above (Prefeasibility) and step 5 (Production), Adriatic Metals has seen about a 4x increase in its stock (42% annualized growth). I’ve marked where SVM is currently for your reference.

Initially, its stock price reflects the cost, and when production starts, it aligns more with its discounted value of future mining cash flows. See the graph below for reference.

With this basis, I’ve performed calculations for SVM.

The Case for SVM

I have created my model and compared it with their prefeasibility study estimates.

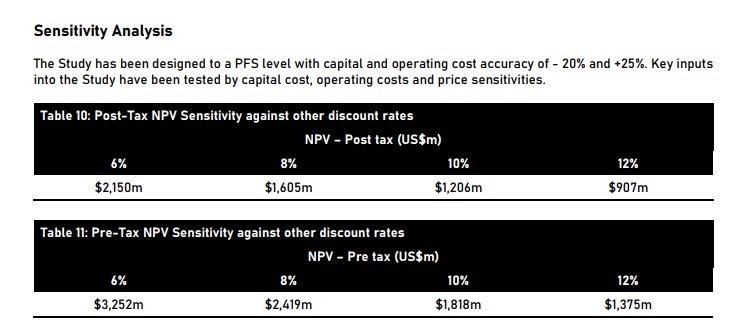

Their prefeasibility model's sensitivities are as follows:

They calculate a NAV of $1600M USD. Deducting 40% for Rio Tinto's right to sell 40% of the production leaves us with an adjusted NAV of $800M USD in the base case. This is over $1250M AUD compared to the current $275-300M AUD, representing a potential 4.5x increase.

Applying a higher discount rate of 12% leaves us with a NAV of $450M and a 2x potential.

In my case, I’ve applied the following parameters based on my understanding of SVM’s business case:

20% higher rutile prices

40% higher graphite prices

10% discount rate (target once built and financed with a long-term structure)

+10% construction cost

+10% operating costs

Construction delay until the end of 2028

The discount should mostly come via debt, at a significantly lower rate than the equivalent risk of Malawi and a mining business.

With this case, we get a NAV around $1800-2000M USD and an adjusted NAV of $900-1000M USD. This is about $1400-1550M AUD versus $275M AUD, representing a potential 6x increase.

Realistically, Africa's risk justifies a higher discount, and the asset should trade at 0.8 times NAV, equating to $1200M AUD, suggesting a 4x potential.

Considering some dilution and financing uncertainties, the return should be between 3x and 4x over 4 years.

As always, remember that these are very indicative estimates, and all estimates are inherently flawed.

Conclusion

Investing in Sovereign Metals means investing in a re-rating from a developer to a producer. The quality of the Kasiya Project, the discount to potential NAV, the cooperation with Rio Tinto, and especially the inclusion of graphite and rutile in the project make it an investment with potential. According to my calculations, it offers a 3x-6x potential, with a CAGR (compound annual growth rate) of at least 30% annually over 4 years.

In my opinion, these factors make Sovereign Metals an attractive option for investors interested in the mining industry and the growth potential of two key elements of the energy transition.